By Campbell Pryde, President and CEO, XBRL US

The failure of Silicon Valley Bank (SVB) was not a surprise to regulators or investors who took the time to check the bank’s financial statements and footnotes. By March of 2021, unrealized debt securities losses for the bank had already begun to climb, reaching ($1,343) million by year-end December 2021, and leaping to ($15,160) million a year later, all the while the bank’s stockholders’ equity remained flat.

SVB, like most public companies, submits financial statements to the Securities and Exchange Commission (SEC) in machine-readable (XBRL) format. Unrealized debt securities losses and stockholders’ equity were easily available in their financials and footnotes. In fact, they were prepared in structured, machine-readable (XBRL) format and thus could be extracted for analysis from the statements within seconds. SVB losses were an obvious red flag and had been for two years.

Loopholes allow variation in how banks disclose financials

While with Silicon Valley Bank, the facts were in plain sight, other banks may be leveraging regulatory loopholes to skirt around disclosure requirements. That could spell more trouble ahead for the banking system.

Most banks file financial statements to both the Federal Deposit Insurance Corporation (FDIC) and the SEC. Financial statements filed with the FDIC follow the bank call report standard for these disclosures, not the US GAAP Accounting Standard which is used for SEC reporting.

Signature Bank (SBNY) closed its doors on March 12, 2023. Although SBNY is publicly traded and therefore subject to SEC regulations, it opted to take advantage of a loophole in securities regulations that allow banks to file Form D, notice of an exempt offering of securities with the SEC. This means that unlike SVB, SBNY did not file financial statements to the SEC, avoiding SEC oversight altogether, and making it less transparent to equity investors.

This seems particularly problematic because not only is Signature Bank publicly listed, but it recently grew large enough to qualify to be included in the S&P 500. In fact, Signature Bank is the second S&P 500 bank that opted out of SEC reporting. Republic Bank did too (see list of banks that file only to the FDIC). This makes it especially challenging for equity analysts and investors to get a real picture of the market as a whole, and banks in particular.

“At Calcbench we have been advocating for a while for FDIC supervised banks to conform to SEC reporting standards. Having not one, but two S&P 500 constituents that did not, for example, file annual and quarterly reports in XBRL format, was not acceptable from a data transparency standpoint,” said Alex Rapp, President of Calcbench, a financial analytics platform.

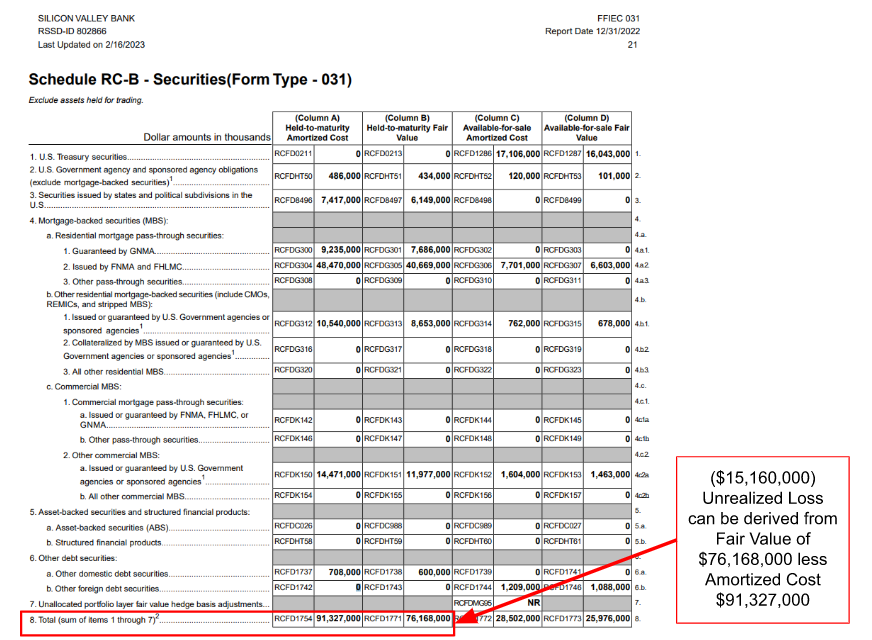

While SBNY continues to submit call reports to the FDIC, the call report does not include the disclosure of unrealized debt securities losses like the SEC financial statement, although it can be derived by calculating it from two figures on the call report as shown on the SVB call report below (click the image for larger view).

If SVB had opted for the Form D loophole like SBNY, and only filed financial statements with the FDIC, the loss would not have been reported on its financial statements, limiting the ability of regulators and equity analysts to catch the problem.

While this is problematic, it also raises the issue that two high-profile banks are disclosing critical information to investors differently. And for equity investors, accustomed to focusing on SEC filings, the ability to opt out of SEC filings completely, is extremely worrisome. This kind of regulatory fragmentation is highly inefficient and costly, both for reporting entities and data consumers.

Authors of the academic study, Fragmented Securities Regulation, Information-Processing Costs, and Insider Trading specifically addressed inconsistencies between bank disclosure requirements between the SEC and the FDIC. They point out, “Our findings suggest regulatory fragmentation adversely affects the market efficiency and level playing field by increasing information-processing costs, a novel mechanism through which regulatory fragmentation creates costs to the financial system.”

Addressing regulatory fragmentation

The Financial Data Transparency Act (FDTA), signed into law in December 2022, calls for the use of data standards by 8 member agencies of the Financial Stability Oversight Council (FSOC), including the FDIC and the SEC. Per the legislation, this must be a coordinated effort between the agencies, with an aim to “... reducing the private sector’s regulatory compliance burdens while enhancing transparency and accountability to the benefit of consumers and investors.”

What better use of the FDTA than to fix the regulatory fragmentation in the banking markets? Coordinating efforts between agencies like the SEC and the FDIC can lessen reporting burden and improve the usefulness of data needed by regulators and investors.

Governments world-wide have taken this approach, and benefited from it broadly, in cost reduction and productivity improvements across reporting entities, regulators, and data consumers.