Ami Beers, Director — Assurance and Advisory Services, Corporate Reporting, Association of International Certified Professional Accountants (AICPA); Member, XBRL US Data Quality Committee

It is that time of year when families and friends gather together to share a meal. I recently hosted Thanksgiving dinner for my entire family. When it comes to preparing the perfect dinner for over 30 people, you have to get it right. The turkey is the most important part, so for the perfectly cooked bird, you need the right tools. Having the right thermometer, baster and pan helped me to ensure that I had a perfectly cooked bird. Family meals can be stressful, the risk of mistakes (such as a dry overcooked turkey) can make for an uncomfortable evening. However, the right tools can help to get it right.

Preparing quarterly financial statements is another activity where “getting it right” is critical. The risk of mistakes has significant downsides, ranging from SEC sanction to negatively affecting your company stock price.

And today, the SEC requires Inline XBRL for operating companies. The downside of errors in the XBRL tagging of a company’s financial statements is even higher. Inline XBRL effectively combines the XBRL and HTML version of corporate financials so that an error in the XBRL data becomes more visible with inline.

But manually reviewing an XBRL filing can be a daunting task. For example, Pfizer’s most recent 10-K, dated February 22, 2018, contained 3,622 individual reported facts. Checking each datapoint to see if the right sign has been used or if the dimension is structured correctly is extremely time consuming by hand.

That’s why the XBRL US Data Quality Committee (DQC) provides the tools that filers need to get their XBRL financial statements right. The DQC creates freely available rules that can be run automatically against a corporate filing, to identify errors and allow filers to resolve them before SEC submission. Automated rules are the most efficient, and perhaps the only feasible way, to provide comprehensive, consistent, automatic checks for issuers to use as a tool to review their filings.

That’s also why the DQC takes such extraordinary care and rigor in the development and creation of these validation rules. Errors in your regulatory filing is too big a risk.

The DQC has published seven rulesets since its inception in 2015. With every ruleset, a stringent 7-step development process is followed in order to ensure that the errors triggered by the rule are true errors that filers need to address before they submit their financial statements.

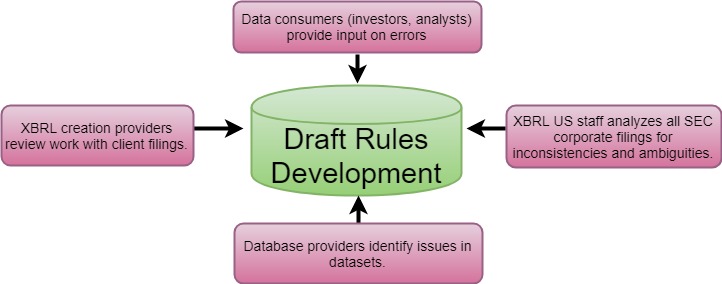

Step 1. Create draft rules.

One problem area is tackled in a single rule, for example negative values (that should be positive), or invalid use of combinations of axes and members. Members of the DQC are corporate issuers, filing agents, database providers, academics, XBRL experts, accountants, and securities analysts, each with different expertise to contribute to the process of drafting rules. Data consumers and analysts provide input on errors they find in filings. Database providers review and weigh in on errors they find in their own datasets. XBRL US staff reviews every SEC-submitted filing to identify mistakes. Filing agents and XBRL tool providers review their work with clients. The DQC also meet with standard setters and regulators on a regular basis to review the draft rules.

Step 2. Consider potential problems with each draft rule.

Once the topic areas are identified and draft rules are developed, the DQC undergoes a process to evaluate the utility of each rule.

What is the impact of the draft rule? Repercussions of an error must be significant enough that it merits flagging to filers.

Does the error occur frequently among multiple filers? It might just be an anomaly that only affected a single filer and therefore may not be worthwhile to include in the ruleset.

Is the rule clear and unambiguous and does the error message provide clear instructions to an issuer? If not, a rule should not be written.

Might the rule result in “false positives”?

Validation rules must be written considering every possible situation. For example, some concepts in the US GAAP Taxonomy should always be reported as positive values, except when certain dimensions are used with these concepts. Instances where dimensions are used may be rare, but it’s important that the rules handle all of these situations. The DQC rule for these kinds of concepts includes a list of exceptions so that if a filer uses one of these concepts without a dimension, he or she will get a negative value warning. But if he or she uses a concept with one of the “exception dimensions”, no warning will be triggered.

Similarly, when a filer uses the 2018 release of the US GAAP Taxonomy, an error flag will appear if he uses a concept that has been deprecated from the 2018 release. But if he is preparing his filing using the 2017 Taxonomy, and that concept was valid for the 2017 release, no error will be triggered.

The DQC vets every rule with this level of care. This is because the risk is too high that a filer will be led astray and waste time attempting to correct something that was right in the first place, and potentially introduce a new error into their filing.

Step 3. Write clear, unambiguous error messages.

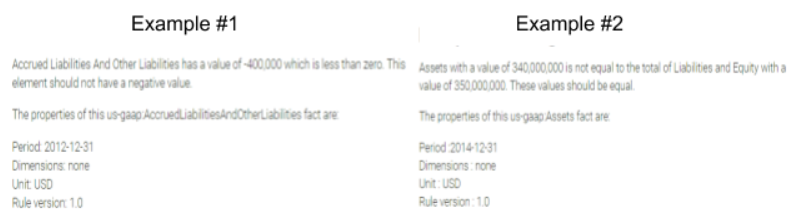

Each rule must provide simple instructions that issuers can easily follow to correct their filing. Any rule that can’t be easily explained simply won’t do. Below are examples of error messages that filers receive when running the rules. These messages explain the error for the incorrect tagging found within a filing. Example #1 states that a fact reported for a certain concept must always be positive. Example #2 states that the value tagged for Assets must equal the value tagged for the element Liabilities plus Equity.

Step 4. Test the rules.

Every draft rule is tested by running it against all historical corporate filings from 2009 to date. Reported values that trigger the draft rule are analyzed to make sure that they are flagging errors appropriately and not generating false positives.

Step 5. Conduct public review of each rule.

The DQC makes all draft rules available to the general public, along with a tool on the XBRL US website (https://xbrl.us/data-quality/rules-guidance/check-filing/) so that filers can run the draft rules themselves to check if their filing (historical or not yet submitted) triggers a draft rule. Issuers can provide feedback to the DQC when an error has been triggered incorrectly or if the error message is not clear. This type of input is invaluable to ensuring that the rules are clear, unambiguous, and accurate at catching mistakes. Issuers, data providers, analysts, filing agents, and accounting professionals are strongly encouraged to review the rules and provide their input.

Step 6. Incorporate market feedback.

After the public review, which usually runs 45 days, all submitted comments are reviewed by the DQC and revisions may be made.

Step 7. Publish the final ruleset.

Once the DQC formally approves the rules, they are made freely available and can be used by filers directly on the XBRL US web site, or are incorporated into filing agent processes and tool provider software.

XBRL US also certifies software that has been proven to successfully run the rules, flagging errors where appropriate. The DQC certification process is equally rigorous. The entire ruleset is incorporated into the software being tested, and run against every historical XBRL SEC filing. Results generated through the software are analyzed to determine if errors are triggered in filings that are known to contain errors. If the results are not accurate, the XBRL US team works with the filing agent or software provider to make corrections, until the rules run smoothly and successfully, producing expected results. Certified software applications can be seen here.

Get your financials right every time. Use the rules.

The XBRL US DQC knows how important your corporate financials are. Being “good enough” is not an option. Just as important as having the right thermometer to cook the perfect Thanksgiving turkey, having the right tools to ensure that your financials are accurate is paramount.

The DQC is funded through the members of the Center for Data Quality.

To learn more about the work of the DQC and the Center, read this white paper:XBRL US Center for Data Quality White Paper