This guidance supersedes the prior guidance "XBRL US Best Practices/Data Quality Working Group- 2.1.5 Multiple Dividends Declared and Paid". Filers are encouraged to modify their tagging following the approach outlined in the new guidance.

This guidance is intended to unify the dividends disclosures between reporting textual disclosures of a dividend event, schedules of dividends paid, the Cash Flow statement, the Statement of Financial Position , the Income Statement and the Statement of Shareholders Equity.

This enables easier checking of disclosures, improved quality and consistency of data and improved ease of tagging.

1.0 Report specific dividends events versus summary dividends information?

When filers report specific dividend events, information such as the declaration date, record date, payment date associated with the dividend amount is generally also presented. When a dividend amount is not reported with associated declaration date, record date, payment date information, it is usually a summary of dividends declared and/or paid (individually or in aggregation) recognized within a specific reporting period.

Example 1: (This is a dividend event)

Example 2: (This is summary dividends information)

Example 3: (This is a combination of dividend events and summary dividends information)

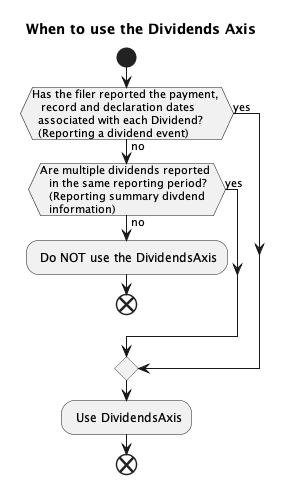

1.1 When should I use the dividend axis?

The DividendsAxis should be used when reporting a specific dividend event, where record date, payment date and declaration date associated with the dividend amount are generally also presented. The DividendsAxis should also be used when reporting summary dividends information, if multiple dividends are reported in the same reporting period (for disaggregation). Filers should also use the DividendsAxis, if the dividend is declared after the reporting period and the dividend can be associated with a particular reporting period. However, the DividendsAxis is not needed if the dividend declared after the reporting period is the annual total of several individual dividends to be paid in the next fiscal period. Examples in section 2.2 and 3.1 of this guidance illustrate the scenarios where DividendsAxis should or should not be used.

Figure 1

1.2 How should members be named on the DividendsAxis?

Use the following format for regular (ordinary) quarterly dividends O2024Q1DividendsMember.

Use the following format for semi-annual dividends O2024H1DividendsMember.

Use the following format for annual dividends O2023ADividendsMember.

For special dividends use S2024DividendsMember.

The syntax that should be followed for the dividend member is as follows:

- Dividend type: Values of either "O" or "S". A value of "O" represents regular (ordinary) dividends and "S" represents special dividends.

- Year: Represented using 4 numerical values

- Period: The period is represented using either Q1, Q2, Q3, Q4, H1, H2, M1, M2, M3 to M13 or the value A for annual dividends.

- Optional alpha characters: This is used to capture additional info to disaggregate the dividend member such as warrant and non warrant portion of dividend. (Do not use for different classes of stock as the class of stock axis should be used).

- Include the word "Dividends".

- Member: The end of the member name must include the string "Member"

Examples:

O2025Q3DividendsMember: A regular quarterly dividend for Q3 in 2025.

O2026ADividendsMember: An annual dividend for 2026.

Additional number/character may be added, if there are multiple dividends declared in the same quarter/month. For example, O2022Q11DividendsMember, O2022Q12DividendsMember, and O2022Q13DividendsMember can be created, if there are 3 separate ordinary dividend events in Q1 2022 for the same class of stock.

Use Class of Stock [Axis] to disaggregate dividends for different classes of stock.

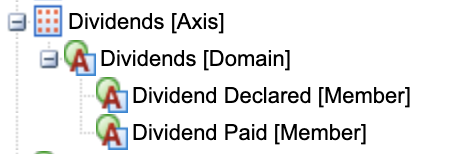

1.3 When should the members (Dividend Declared [Member] and Dividend Paid [Member]) be used?

The US GAAP taxonomy includes the members Dividend Declared [Member] and Dividend Paid [Member].

In the disclosure below these members may seem to be a reasonable way to tag the data. However, the more appropriate approach is to tag the values in each of the columns using the specific dividend elements (see detail tagging in 3.1, Example 4). These members should not be used.

1.4 Should the record date, payment date and declaration date associated with the dividend amount be tagged?

The SEC makes the tagging of dates voluntary, but it is recommended that dividend dates are tagged to get the advantage of having more effective validation of your filing and that these dates are critical for investors.

1.5 What context should be used to tag the record date, payment date and declaration date associated with a dividend announcement?

All dividend dates reported should be tagged with a unique member (such as O2023Q1DividendsMember) on the DividendsAxis. The date context period should align to the date context used for tagging CommonStockDividendsPerShareDeclared/ PreferredStockDividendsPerShareDeclared).

In a subsequent event disclosure, when the dividend 'payable' elements are used (instead of CommonStockDividendsPerShareDeclared/ PreferredStockDividendsPerShareDeclared), the date content for tagging dividend dates would be the duration from the period-end to the declared date (see section 2.2, Example 2).

2.1 When are the DividendsPayableAmountPerShare and DividendsPayableCurrent used (or DividendsPayableCurrentAndNoncurrent for an unclassified Balance Sheet)?

These elements are instant period type and the value reported should reflect the value of dividends payable (per share or dollar amount) at a given point in time. DividendsPayableCurrent and DividendsPayableCurrentAndNoncurrent should be used to report the dividends payable appearing on the balance sheet.

If the dividends announced are associated with multiple dividends in future periods and the total dividends to be paid is reported as shown in section 2.2, example 2, then the element DividendsPayableAmountPerShare should be used.

2.2 What date context and element should I use to tag the details of dividends declared after the period year end?

Example 1: (For annual reporting period end of 12/31/2022)

The value of dividends declared ($0.20) after the period end should use the element CommonStockDividendsPerShareDeclared and should have a date that corresponds to the report year end to the declared date (02/15/2023), together with a unique member (O2023Q1DividendsMember) on the DividendsAxis because the dividend represents a specific dividend event.

While the SEC makes the tagging of dates voluntary, it is recommended that dividend dates are tagged, as these dates are critical for investors.

In this example, filers can also tag DividendsPayableDateDeclaredDayMonthAndYear (value 2023-02-15), DividendsPayableDateOfRecordDayMonthAndYear (value 2023-03-01) and DividendPayableDateToBePaidDayMonthAndYear (value 2023-03-15), with the duration from the period-end date to the declared date. The date values need to be tagged with the O2023Q1DividendsMember on the DividendsAxis.

Values reported should include the subsequent event axis if they are disclosed as a subsequent event.

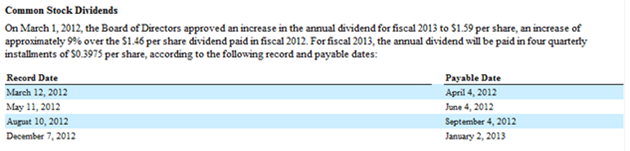

Example 2: (For annual reporting period end of 1/31/2012)

The value of $1.59 would be tagged with element DividendsPayableAmountPerShare with the date March 1, 2012. This would not have a dividend member as it represents the sum of 4 dividends. The value of $0.3975 is tagged 4 times using the element CommonStockDividendsPerShareDeclared. The DividendsAxis should be used to separate these 4 values with unique members (O2013Q1DividendsMember, O2013Q2DividendsMember, O2013Q3DividendsMember, and O2013Q4DividendsMember) that are specific to the dividend. The date context should be the duration from the period-end date to the declared date.

Filers can also tag dividend dates (DividendsPayableDateOfRecordDayMonthAndYear and DividendPayableDateToBePaidDayMonthAndYear), with the duration from the period-end date to the declared date. The date values should be tagged with the 4 unique members on the DividendsAxis.

The value $1.46 is tagged with the element CommonStockDividendsPerShareDeclared as it represents the expense per share. The context period should be 12 months ended January 31, 2012. The DividendsAxis should not be used for the value $1.46 (see 3.1).

3.1 When and how is CommonStockDividendsPerShareDeclared (per share amount) and DividendsCommonStock (total dollar amount) used?

The value of CommonStockDividendsPerShareDeclared represents the DividendsExpense for the period divided by the number of shares. The date context period should equal the period where the dividend expense was recognized. This allows the comparison to other metrics such as earnings per share and to check if the CommonStockDividendsPerShareDeclared matches the dividend expense recognized in the period.

The DividendsAxis should be used when reporting a specific dividend event, where record date, payment date and declaration date associated with the dividend amount are generally also presented.

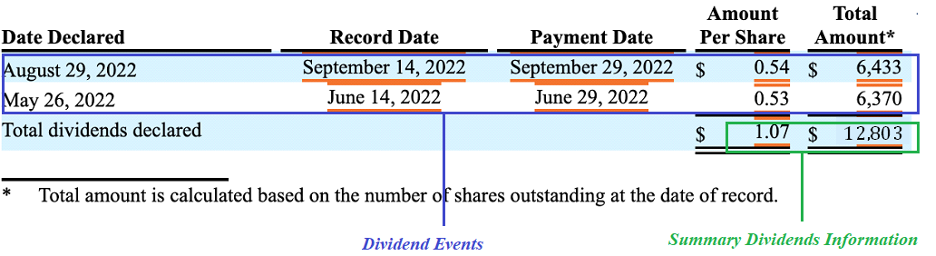

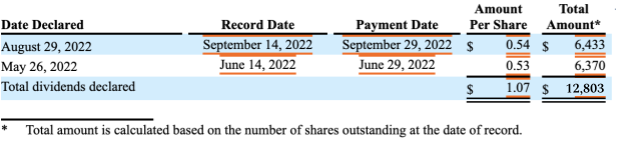

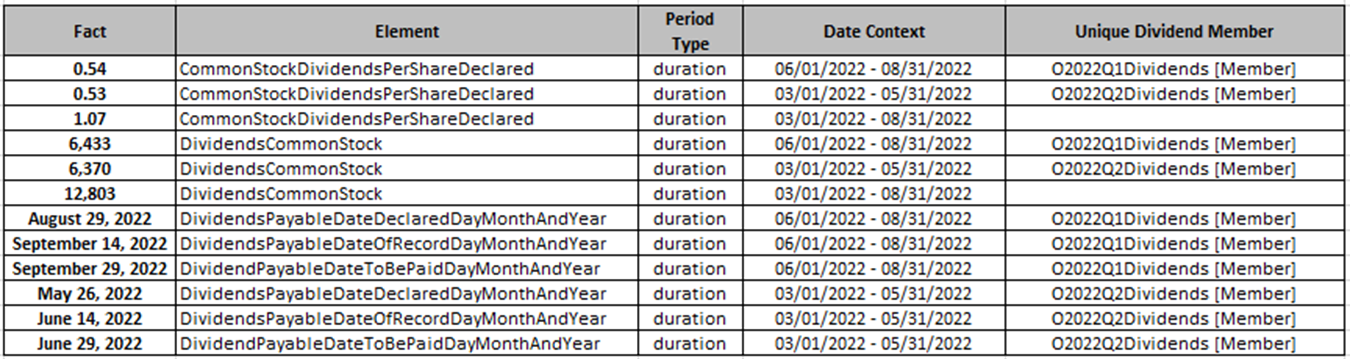

Example 1: (For Q2 reporting period end of 8/31/2022)

Figure 4

In this example, $0.54 and $0.53 or $6,433 and $$6,370are individual dividend events, unique members on DividendsAxis are required. $1.07 (or $12,803) are summary dividend information (see section 1.0), DividendsAxis is not required. The date context for non-numeric facts should align to the period used for tagging CommonStockDividendsPerShareDeclared.

The element DividendsCommonStock (representing paid and unpaid dividend) is used to tag the "Total Amount" column in this example, because the Q2 dividends remained unpaid at the end of the 8/31/2022 reporting period.

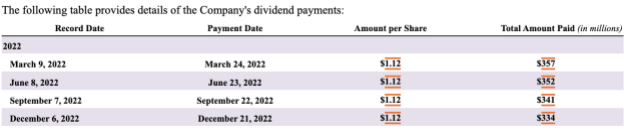

Example 2: (For annual reporting period end of 12/31/2022)

In this example, the dividends per share value of $1.12 should be reported using the element CommonStockDividendsPerShareDeclared, and the value for total amount paid should use the element PaymentsOfDividendsCommonStock. The values should be tagged to the period context for the period in which the dividend expense was recognized, and the payment was made (i.e., Q1, Q2, Q3, Q4).

Unique members on DividendsAxis are required because dividend events (with dividend dates) are reported (see 1.0). The date context for these non-numeric facts should align to the period used for tagging CommonStockDividendsPerShareDeclared.

The element PaymentsOfDividendsCommonStock (representing paid dividend) is used to tag the "Total Amount Paid" column in this example, because all dividends were paid before the end of the 12/31/2022 reporting period.

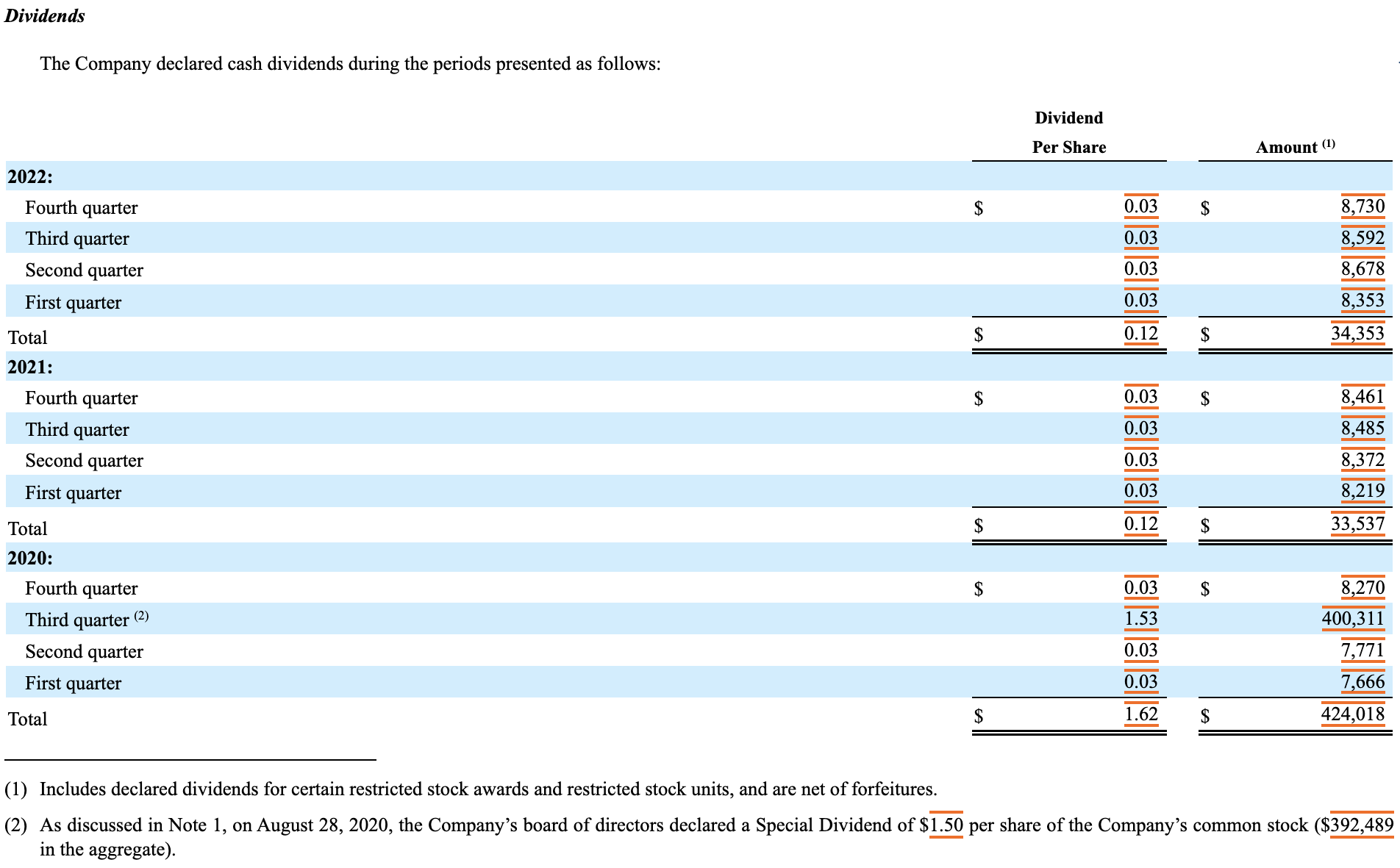

Example 3: (For annual reporting period end of 12/31/2022)

In this example, the values of the two columns would be tagged using the elements CommonStockDividendsPerShareDeclared and DividendsCommonStock. There is no dividend date information associated with the dividend announcement. This is summary dividend information (see section 1.0). These individual dividends can be tagged (without the use of unique members on the DividendsAxis) to different context dates matching dividend expenses recognized in the period (Q1, Q2, Q3, Q4, and Annual).

The element DividendsCommonStock (representing paid and unpaid dividend) is used to tag the "Amount" column in this example, because it is unclear whether all dividends have been paid at the end of the 12/31/2022 reporting period.

However, in 2020 a special dividend was declared of $1.50. This value would require the use of the DividendsAxis to distinguish it from the value of $1.53 in the 3rd quarter of 2020. The value of $1.53 would not use the DividendsAxis but the values of $1.50 and $392,489 would. These values would use the member S2020Q3DividendsMember.

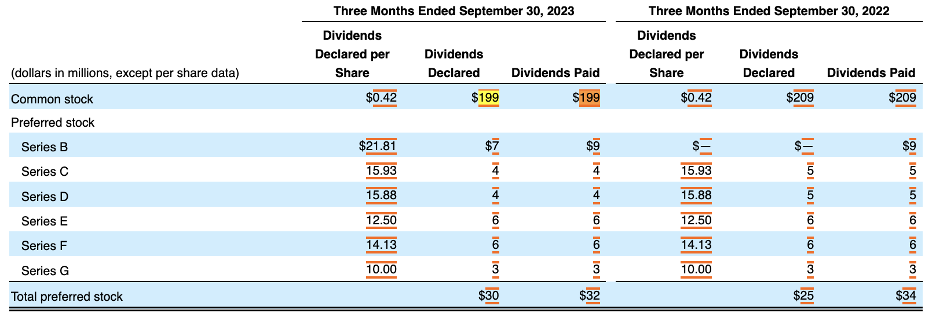

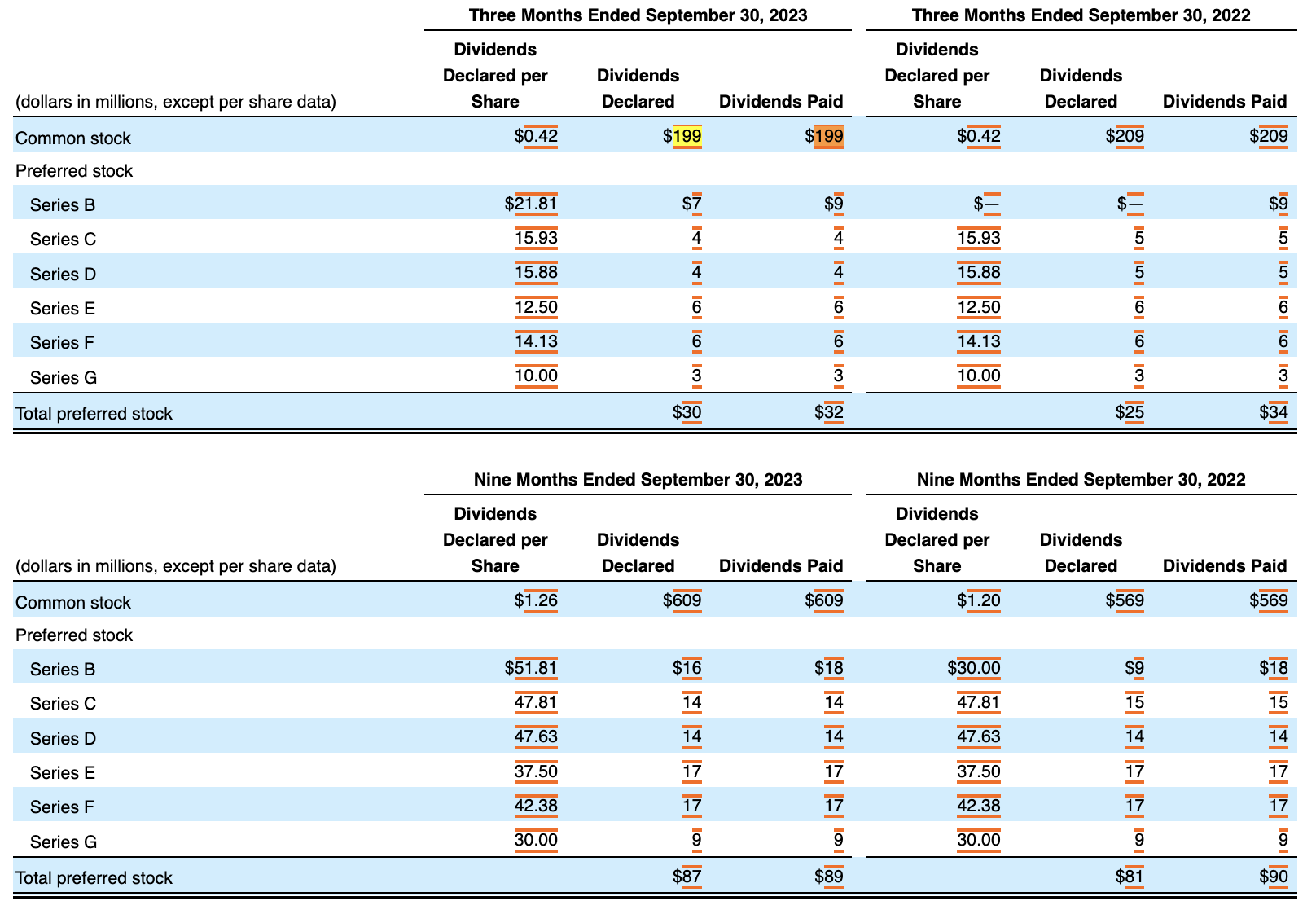

Example 4: (For Q3 reporting period end of 09/30/2023)

In this example, the first column should be tagged with the elements CommonStockDividendsPerShareDeclared and PreferredStockDividendsPerShareDeclared. If the dividends are paid entirely in cash and are the same amount then the elements CommonStockDividendsPerShareCashPaid and PreferredStockDividendsPerShareCashPaid could be used. The PreferredStockDividendsPerShareDeclared elements should be disaggregated using the ClassOfStockAxis.

The second column showing "Dividends Declared" should use the elements DividendsCommonStock and DividendsPreferredStock or the more specific elements CashDividendsCommonStockCash and DividendsPreferredStockCash for each class of preferred stock.

The third column representing "Dividends Paid" should have used the elements PaymentsOfDividendsCommonStock for the payments of dividends for common stock and PaymentsOfDividendsPreferredStockAndPreferenceStock for preferred stock with the ClassOfStockAxis. The context of the periods should have been 3 months for the top schedule and nine months for the bottom schedule. Do not use the two standard members (Dividend Declared [Member] and Dividend Paid [Member]) on the DividendAxis (see 1.3).

Note that the DividendsAxis is not used for this disclosure. When dividend disclosures are not associated with a specific dividend event then the DividendsAxis is not used.

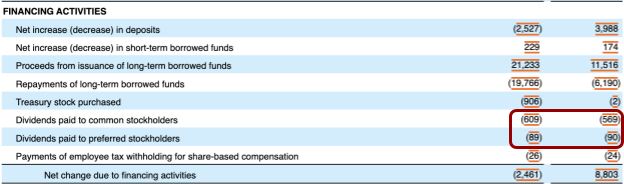

The use of these elements then correspond to the disclosure on the cash flow statement:

The values for $609 and $89 tie back to the values in the dividend schedule. This means the same values are tagged with the same element and the same context.

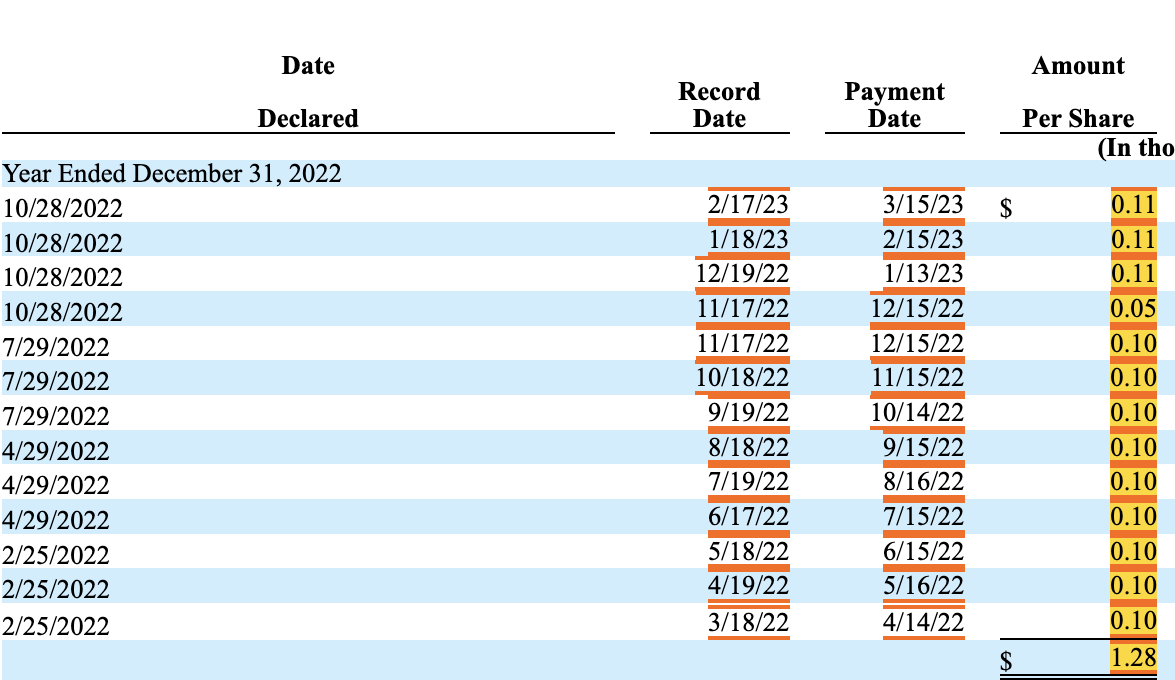

Example 5: (For annual reporting period end of 12/31/2022)

In this example, we use the element CommonStockDividendsPerShareDeclared. There are multiple dividends reported in the same filing period (annual reporting period) and the expense period (Q1, Q2, Q3, or Q4) for each dividend is not clearly presented. The period context of each dividend amount should be tagged with a 12-month period and is disaggregated using the DividendsAxis.

Unique members on DividendsAxis are required (except for the total $1.28), because individual dividend events (with dividend dates) are reported. The date context for these non-numeric facts should align to the period used for tagging CommonStockDividendsPerShareDeclared.

4.1 What elements should be used to report dividends declared per share, reported in the income statement?

The element CommonStockDividendsPerShareDeclared with the period context aligning to each fiscal year is used.

4.2 What element should be used to report dividends or distributions payable in the supplemental section of the cash flow statement?

The element DividendsPayableCurrent (DividendsPayableCurrentAndNoncurrent for unclassified balance sheet) should be used to report Distributions payable ($9,159). In the case of investment companies the element DistributionPayable could also be used if it includes distributions other than dividends. Companies should not create extensions for this element that are a duration. The amount reported in the cash flow statement should correspond to the value reported on the balance sheet.

4.3 What element should be used if dividends are paid out of additional paid in capital?

In some cases, filers pay dividends when there is insufficient funds in retained earnings to cover the distribution. Filers should use the element AdjustmentsToAdditionalPaidInCapitalDividendsInExcessOfRetainedEarnings (instead of a regular dividend element like DividendsCommonStock or DividendsCommonStockCash) to tag the dividends line ($18,576) in the example below.

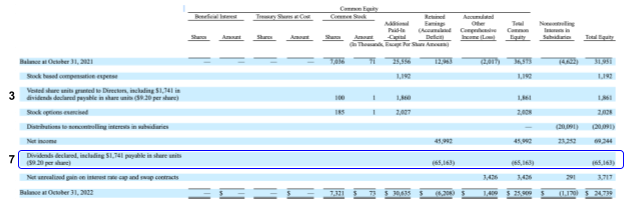

4.4 How are combined cash and stock dividends represented in the Statement of Changes in Shareholders Equity?

In this example, the value of dividends declared on line 7 represents dividends that will be paid in cash and in stock. Line 3 contains the details about the impact of the stock issuance on APIC and common stock for the dividends on line 7 and offsets line 7. Line 7 reports the impact on retained earnings. Because the retained earnings will be distributed between cash and stock the most appropriate element to use is DividendsCommonStock for line 7. The DQC rules check if the value of the DividendsCommonStockStock combined with the retained earnings member is the same as DividendsCommonStockStock with no member on the Equity components axis to detect inappropriate use of the DividendsCommonStockStock element.

View: as part of approved release master || public exposure version & comments.

Data Quality Rules

Latest Rules (works with Arelle)

Developer Resources

- DQC Rules Validator (part of the XULE plugin for Arelle)

- XULE Editor extension for Visual Studio Code (What is XULE?)

- DQC Reference Implementation Code

Travis CI status -

- Global Rule Logic